SHA claims Proxy Means Testing shields low-income Kenyans. A closer look at its own data suggests most informal-sector households are paying more than they ever did under NHIF.

The debate over SHA means testing has become increasingly polarised. The Social Health Authority (SHA) and the Ministry of Health (MoH) argue that Proxy Means Testing (PMT) is necessary to promote equity and financial sustainability. Critics, including industry stakeholders, analysts and patients, argue that it is exclusionary and poorly suited to Kenya’s informal economy.

The reality is more complex.

SHA, in a press statement on PMT published on May 6, 2026, raises some valid concerns about weaknesses in the National Hospital Insurance Fund (NHIF) model. However, several of its central claims become less convincing when tested against official data, the Auditor-General’s findings, Kenya’s legal framework, and international experience.

This article is part of a series of three articles that will examine six key questions:

- Did SHA reduce dependence on formal workers?

- Are poorer households actually paying less?

- Is PMT truly global best practice?

- Are appeals and dispute mechanisms accessible?

- Is PMT suitable for Kenya’s informal economy?

- Does the Primary Healthcare Fund (PHCF) solve the affordability problem for the informal poor and near-poor?

Finally, we will consider what Kenya can do differently. But first, let’s explore SHA’s informal sector problem where numbers tell a different story.

The first issue to ask is:

Did SHA correct NHIF’s over-reliance on formal-sector contributors?

The SHA statement argues that moving from NHIF to SHA was necessary because NHIF had structural weaknesses and equity gaps. Specifically, it says NHIF depended heavily on the roughly 20 per cent of Kenyans in formal employment to finance healthcare for the wider population, making the system both unsustainable and unfair. SHA also insists that NHIF’s contribution model was regressive and inconsistent with the principles of social health insurance and risk pooling.

Well, we can concede one point to SHA: Under NHIF, salaried workers contributed on a graduated scale, but payments were capped at Ksh1,700 per month for anyone earning Ksh 100,000 or more. By contrast, self-employed and informal-sector members paid a flat Ksh500 per month. As a result, high-income formal-sector workers contributed only a small fraction of their income.

For example, someone earning Ksh1,000,000 per month and paying Ksh1,700 contributed just 0.17 per cent of their income, while a self-employed person earning Ksh10,000 and paying Ksh 500 contributed five per cent. In this limited sense, SHA’s criticism is valid: NHIF’s structure was regressive at both ends, placing a heavier burden on some low-income informal workers while allowing high-income salaried workers to contribute proportionately less. But this is as far as the concession goes.

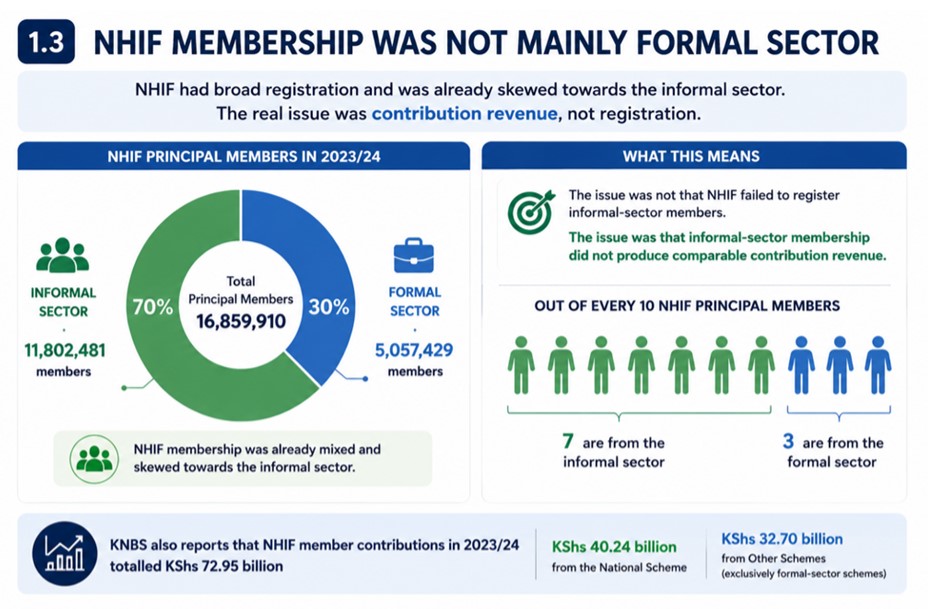

Was NHIF membership mainly from the formal sector?

SHA implies that NHIF’s financing structure discriminated against and largely left out the informal sector, yet according to the KNBS Economic Survey 2025, NHIF had 16,859,910 principal members and 15,481,530 dependents in 2023/24, for total registered coverage of 32,341,440 people.

Of the principal members, 5,057,429 were from the formal sector, while 11,802,481 were from the informal sector. Put differently, the formal sector accounted for about 30 per cent of NHIF principal membership, while the informal sector made up roughly 70 per cent.

The issue, therefore, was not that NHIF failed to register informal-sector members; rather, informal-sector membership did not produce comparable contribution revenue.

KNBS also reports that NHIF member contributions in 2023/24 totalled Ksh72.95 billion, including Ksh40.24 billion from the National Scheme and Ksh32.70 billion from Other Schemes. KNBS notes that the Other Schemes were exclusively formal-sector schemes offering benefits in addition to the National Scheme. It is therefore clear that NHIF’s membership base was already mixed and, in fact, skewed towards the informal sector.

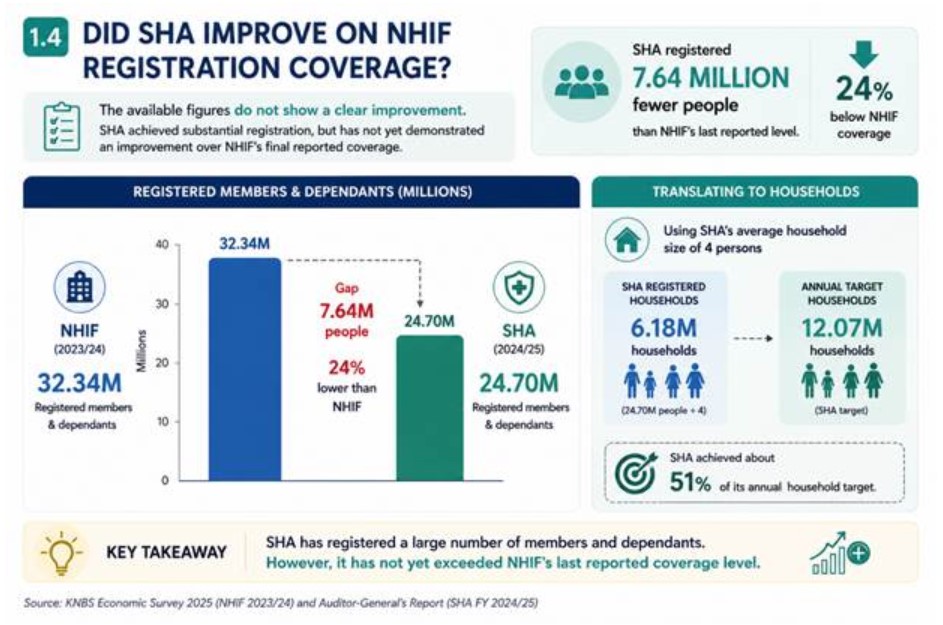

Did SHA improve on NHIF registration coverage?

The available figures do not show a clear improvement.

According to the Auditor-General’s report, SHA had registered 24,702,971 members in FY 2024/25, including 8,427,130 dependants. Using SHA’s average household size of four, this translates to about 6,175,743 households, compared with an annual target of 12.07 million households.

By comparison, NHIF reported total registered coverage of 32.34 million people in 2023/24. On that basis, SHA’s 24.70 million registered members and dependants were about 7.64 million fewer people, or about 24 per cent below NHIF’s last reported coverage level.

This does not mean SHA will not catch up eventually. It simply means claims of improvement should be made cautiously. For now, the more accurate conclusion is that SHA has achieved substantial registration, but it has not yet demonstrated an improvement over NHIF’s final reported coverage.

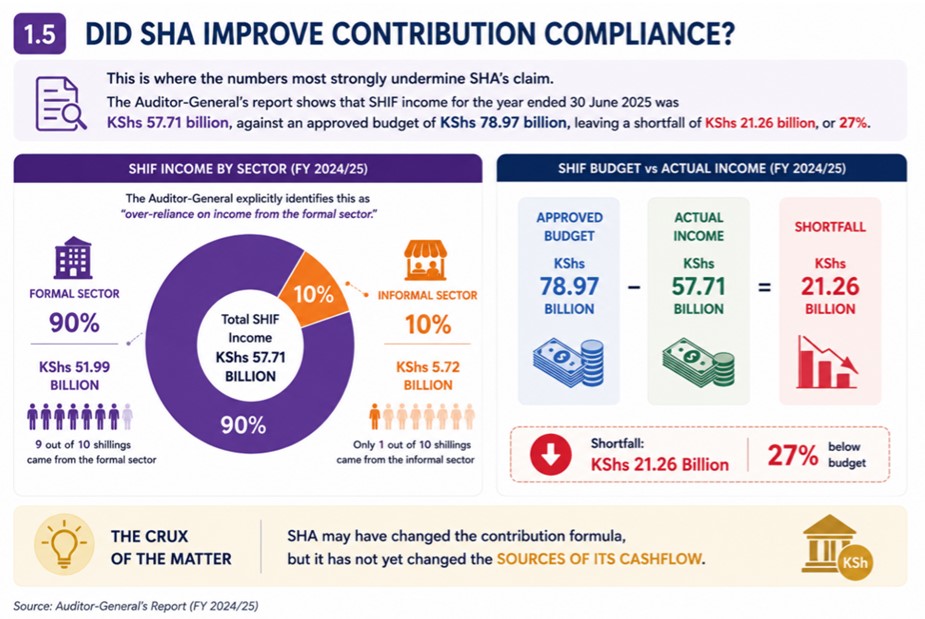

Did SHA improve contribution compliance?

This is where the numbers most strongly undermine SHA’s claim. The Auditor-General’s report shows that the Social Health Insurance Fund (SHIF) income for the year ended June 30, 2025 was Ksh57.71 billion against an approved budget of Ksh78.97 billion. That left a shortfall of Ksh 21.26 billion, or 27 per cent.

More importantly, the same report shows that Ksh51.99 billion, or 90 per cent, came from the formal sector, while only Ksh5.72 billion, or 10 per cent, came from the informal sector. The Auditor-General explicitly identifies this as over-reliance on income from the formal sector.

The crux of the matter is: SHA may have changed the contribution formula, but it has not yet changed the sources of its cash flow.

The interpretation is that SHA may have corrected one weakness in NHIF’s design: the low contribution cap for high-income salaried workers. By moving to a 2.75 per cent income-based contribution, SHA requires high earners to pay more than they did under NHIF.

But that is not the same as solving the pooling problem. The early SHA figures point to three conclusions:

- NHIF already had broad registration coverage, with 32.34 million registered members and dependents in 2023/24.

- SHA had not yet exceeded NHIF’s coverage, with 24.70 million registered members and dependents in FY 2024/25.

- SHA remains heavily dependent on formal-sector contributions, with 90 per cent of SHIF income still coming from the formal sector.

Registration, then, is not the issue. The issue is conversion: turning registration into active, regular contributions, especially in the informal sector.

Are poorer households now paying less under SHA than they did under NHIF?

In its press statement, SHA claims that although no predictive model is perfect, its operational data show that the Proxy Means Testing system “overwhelmingly protects low-income earners.” SHA states that 92 per cent of informal-sector households have been assessed at Ksh850 or less per month, with 45 per cent falling in the Ksh300–500 band and 47 per cent in the Ksh501–850 band. Only 7.1 per cent are placed in the Ksh1,001–3,499 band, while just 0.4 per cent are assessed above Ksh3,500.

On face value, that sounds reassuring. But the claim depends heavily on the new benchmark that SHA has set: The correct benchmark is not Ksh850 – it is Ksh500

Under NHIF, self-employed and informal-sector contributors paid a flat Ksh500 per month. Therefore, the relevant comparison is not whether households are paying less than Ksh850, but whether they are paying less than the previous NHIF contribution of Ksh500.

Only about 45 per cent of assessed informal-sector households appear to pay the same as, or less than, they did under NHIF. At least 54.5 per cent appear to pay more than the previous NHIF flat contribution. This is the opposite of the impression created by SHA’s framing.

The statement that 92 per cent are assessed at Ksh850 or less is technically true, but it subtly shifts the benchmark upward from NHIF’s Ksh500 to SHA’s Ksh850 ceiling. Yet Ksh850 is itself 70 per cent higher than Ksh500.

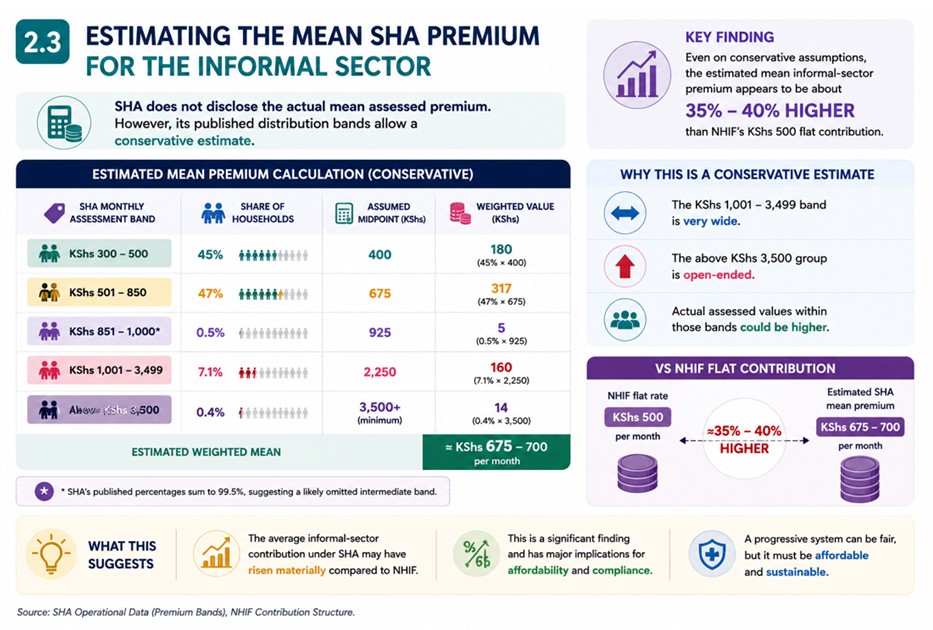

In estimating the mean SHA premium for the informal sector, SHA does not disclose the actual mean assessed premium. However, its published distribution bands allow a conservative estimate.

Using approximate band midpoints, the weighted mean premium is approximately Kshs675–700 per month.

This estimate is conservative for three reasons:

- the Ksh1,001–3,499 band is very wide;

- the above Ksh3,500 group is open-ended;

- actual assessed values within those bands could be higher.

Even on these conservative assumptions, the estimated mean informal-sector premium appears to be about 35–40 per cent higher than NHIF’s Ksh500 flat contribution. This is an important finding.

What SHA’s numbers suggest is that its own operational data do not show that poorer households are in general paying less than before. Instead, the data suggests three things:

- some households are paying less;

- many households are paying more;

- the average informal-sector contribution may have risen materially.

This does not automatically mean SHA is wrong. A progressive financing system can legitimately require higher contributions from households assessed as better off.

The deeper problem is that SHA’s claim only tells us how premiums were assessed. It does not tell us:

- Whether households assessed at Ksh501–850 are genuinely able to pay more;

- Whether households assessed at Ksh300–500 are in fact the poorest households;

- How many households have appealed;

- How many have actually paid;

- How many have lost access because they could not pay;

- Whether households classified as indigent are being subsidised by government;

- Whether treating adult household members as separate contribution units increases the total family burden.

Without this information, SHA’s distribution statistics are an incomplete story. They show what households were assessed, but not whether the assessments are economically realistic, socially sustainable, or operationally successful.

The contribution-compliance problem is such that affordability is not only about what households are assessed to pay. It is also about whether they can realistically pay.

The Auditor-General’s early SHIF figures reinforce this concern: 90 per cent of SHIF income came from the formal sector, while only 10 per cent came from the informal sector. While this does not conclusively imply that premiums are unaffordable, it is firm evidence that assessment is not translating into broad informal-sector payment.

Another problem that SHA’s framing did not fully address is household fragmentation. Under NHIF, a single contributor could cover a spouse and children. Under SHA, however, adults over 18 who are not recognised dependents increasingly become separate contribution units, and adults over 25 without income may still face minimum contribution obligations under the regulations.

This means that a lower premium for one individual does not necessarily reduce the total burden on the household.

A family that was previously covered through one NHIF contribution may now face either multiple Ksh300 minimum contributions or multiple means-tested obligations across adult members.

This hits lower-income households hard, especially those with:

- Unemployed adult children;

- Separated spouses;

- Multi-generational living arrangements; or

- Unstable informal incomes.

In practice, SHA may have lowered some individual premiums while simultaneously increasing the total contribution burden borne by the household.

A fair reading of the available evidence points to a more qualified conclusion. SHA is right on some points. NHIF’s flat-rate structure did contain inequities, and some poorer households now appear to pay less than they did under NHIF. But the broader picture is less favourable to SHA’s overall claim, and whose own figures suggest that:

A majority of informal-sector households may now pay more than NHIF’s Ksh500 flat contribution.

- The estimated mean informal-sector premium under SHA is roughly Ksh675–700 per month;

- The available evidence does not support the claim that the MTI “overwhelmingly protects” low-income earners;

- Weak informal-sector contribution performance may itself point to affordability or assessment problems; and

- Household fragmentation may further increase the effective burden on lower-income families.

The fairest conclusion, therefore, is not that SHA’s argument is entirely wrong. It is that the available evidence does not yet justify the confidence with which SHA has made its claims.

Dr Brian Lishenga is a Family Physician and Chair, Rural & Urban Private Hospitals Association of Kenya (RUPHA)